What Happened to Stitch Fix? Part 1: From Profitable Niche to $100B Disruption Dreams

While the rise of Stitch Fix was well documented, its fall was largely ignored. Dismissed as another post-Covid e-commerce flameout. It's a shame, because the story carries useful lessons. Part 1.

An iconic tweet of the 2020 SaaS euphoria period predicted Stitch Fix becoming a 100-billion-dollar company by 2030:

The stock surged from a $2B valuation to $11B within the next six months. Then it started crashing, completing a 95% post-Covid drop, and never bounced back.

Stitch Fix doesn’t seem to be on track to hit $100B; at this point, getting to a single-billion-dollar valuation by 2030 would be considered a success.

What happened?

This isn’t just another story about investors losing their mind over “digital transformation” stocks during Covid.

What makes this story so painful is that during 2021, the company voluntarily blew up its own business in the span of a few months.

While the rise of Stitch Fix was well documented, its fall was largely ignored. Lumped in with the broader post-Covid e-commerce reckoning. Which is a shame, because this particular story carries some important lessons.

Before answering the question of what happened to Stitch Fix – which I’ll keep for the next post – this article dives into the early success, and what led investors to believe this could be a $100B company.

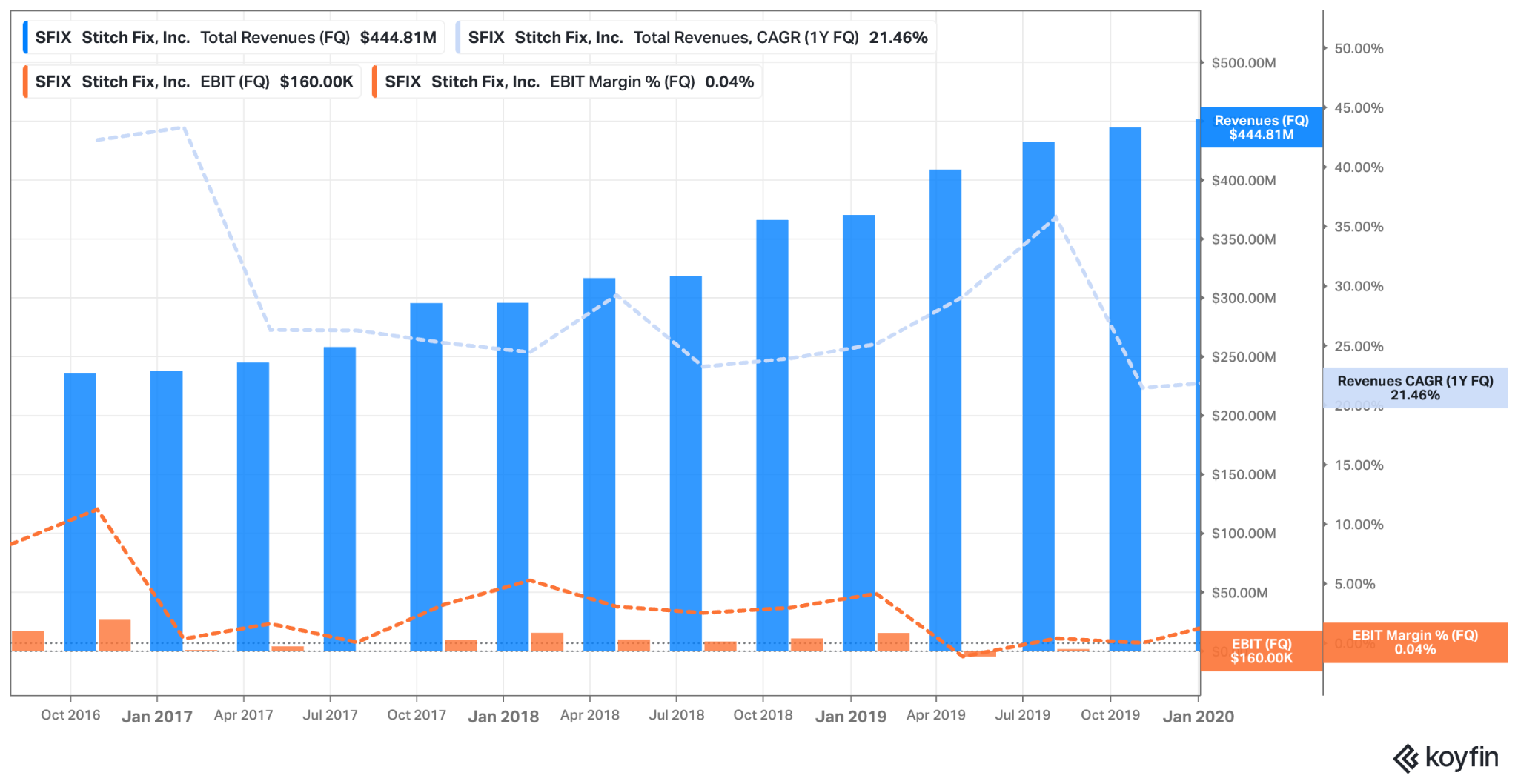

Capital-Efficient Growth

A 2016 Forbes article defined Stitch Fix as “a startup playing Fashionista Moneyball”, but the clothes-matching algorithm was just one of several unique aspects about the company. Founder Katrina Lake scaled and optimized the operation to service the concept of a fix: a box containing five items, selected by a human stylist working with a data-driven system; the customer receiving the box then decides which of the five items they (mostly, she) wishes to actually purchase. The fulfillment centers, software systems, and vendor agreements were all architected around one thing: the five-item box. Thousands of stylists acted as human-in-the-loop curators. Videos of excited customers1 unboxing their mystery fix delivery provided free marketing. Lake’s inspiring story was told in Bill Gurley’s famous Runnin’ down a Dream talk (alongside Bob Dylan and Danny Meyer) in 2018, and subsequently in several popular podcasts.

Many impressive tech companies went public in the late 2010s, though. What made Stitch Fix stand out was how capital-efficient its growth was. Ben Thompson wrote when the company went public in 2017:

In stark contrast to many would-be aggregators, Stitch Fix has taken a shockingly small amount of venture capital — only $42.5 million. Instead the company has been profitable — on an absolute basis in 2015-2016, and quite clearly on a unit basis (including acquisition costs) throughout — and cash flow positive. That increased marketing expenditure is being paid by current customers, not venture capitalists. To that end, a $2 billion IPO would be a massive win for Stitch Fix’s investors and Katrina Lake, the founder.

Moreover, while Stitch Fix’s growth may be slowing, that is by no means fatal: the company is a perfectly valid business to own exactly as it is. Indeed, I am in fact deeply impressed by Stitch Fix: it seems quite clear that early on Lake realized that the company was not an aggregator, which meant building a business, well, normally. That means making real profits, particularly on a unit basis.

[...] Google and Facebook are dominating digital advertising, Amazon is dominating undifferentiated e-commerce, Microsoft and Amazon are dominating enterprise, and Apple is dominating devices. To compete with any of them is an incredibly difficult proposition; better to build a real differentiated business from the get-go, and that is exactly what Stitch Fix did.

More Than Another Subscription Box

Stitch Fix built a durable and profitable business without thinking it had to conquer a huge market. The service didn’t work for everyone, and many customers churned after a single order. But this was fine thanks to Stitch Fix’s focus on unit economics. It made little money on the churned customers, and lots of money on those who fell in love with the service and kept ordering. Mostly it was millennial suburban college-educated women. They had the desire to dress well and enough disposable income to spend, but were often busy and struggled with shopping in stores with endless shelves and small fitting rooms. They felt comfortable with the internet, and enjoyed the experience of receiving a curated shipment to try at their home.

Following the 2017 IPO (and up until the Covid craziness), the market was largely discounting Stitch Fix as yet another money-losing subscription-box business. Most of them optimized for growth by burning investors’ money to subsidize customers. Living in San Francisco back then, I often took advantage of “special offers” made by meal-kit-in-a-box services (why not let a VC pay for my dinner), and usually cancelled right after. Stitch Fix, however, was different, thanks to its early focus on unit economics. And due to not having investors’ money to burn to begin with2.

While closely looking after its profit, Stitch Fix had always been testing ways to expand its market. It experimented with fixes for men and kids, for example, counting on loyal female customers who also wanted the rest of their family to dress well. It also launched its service in the UK. Unit economics, however, didn’t initially work in these new verticals. While the fix model worked well for suburban US females, that fit didn’t immediately translate beyond that core market. A prudent allocator of capital, Stitch Fix limited these growth investments until it could sort out the economics.

From Fixes To Direct Buy

In 2019 Stitch Fix broke out of the 5-items-in-a-box model when it started to introduce direct-buy offerings. Initially dubbed “Shop Your Look”, a testing group of customers were offered – based on their order history – accessories to match their outfits, or more colors of a previously purchased item. It was another attempt to layer new growth s-curves.

To lead the direct-buy expansion, Elizabeth Spaulding was hired as president of Stitch Fix in January 2020. Lake, it seemed, would keep running the core and mature fix business, while overseeing the growth initiatives – now managed by Spaulding – with the usual zeal toward unit economics and profitability.

Direct-buy inspired the idea of Stitch Fix disrupting all of shopping. It was part of the aforementioned “$100B company” Twitter thread:

Eventually Stitch Fix could start ramping up product lines outside apparel in jewelry, home goods, and more. It already knows what customers want. This significantly increases it what it can recommend, the size of the market, ARPU, margins, order frequency, data collection, etc.

Stitch Fix’s “Style Pass” is a $49/mo subscription that collects cash upfront while anchoring customers to making purchases. As it adds product types, it can start shipping clients more than just clothes, increasing revenue per order on the “fixed” shipping costs it’s incurring.

But the personalized marketplace concept was still only an aspirational vision, not a concrete playbook. Until Stitch Fix held its December 2020 earnings call. That’s when – while brick-and-mortar apparel stores were struggling – Lake reported an acceleration in active clients and overall revenue growth. The market was losing its mind. Stitch Fix had often been compared to Netflix – due to its reliance on data and algorithmic-based personalization – and this seemed like the Blockbuster moment for brick-and-mortar apparel.

Then Spaulding elaborated on the progress with direct-buy. Style Shuffle – a ‘Tinder for clothes’ game inside the Stitch Fix app – was gaining strong engagement, and the data it collected enabled the company to launch ‘Shop By Category’ in beta. Which was, essentially, a personalized marketplace for clothes. The prophecy, it seemed, was becoming a reality.

Online commentators (who were many during the Covid lockdowns) were bringing up the Netflix transition into streaming as an analogy for Stitch Fix offering direct buy. The 5-items fix boxes were simply the first act, just like Netflix started with mailing DVDs.

The stock surged 42% the following day, completing a 7x jump(!) from the Covid trough to the post-December earnings peak.

The fall came shortly thereafter.

More on that in the next post.

Subscribe here for it to land directly in your mailbox:

Not financial advice. This post is for educational and general purposes only and should not be relied upon for investment decisions.

Lake was also early to realize the potential of social networks for guerrilla marketing: she used to reach out to influencers on Instagram, offering that they try Stitch Fix. Some would then spread the word to their followers.

In several occasions, Lake elaborated on her struggles to raise money, being a female founder of a fashion startup, in a male-dominated VC ecosystem. That was a key driver of what led her to build Stitch Fix as a bootstrap, using the company’s own profits to fund its growth.