The Turnaround Trap: When the Moat Dries Up

A decades-old lesson from Warren Buffett, that investors seem to keep ignoring.

“Berkshire is a delight to own,” 35-year-old Warren Buffett wrote to his partners in 1965; twenty years later, however, he shut down its original operations, calling it one of the biggest mistakes of his career. The story and the lessons have been well-documented by now, and yet, public market investors keep repeating the same mistake.

“Berkshire is a delight to own”

Both our operating and investment experience cause us to conclude that “turnarounds” seldom turn.

- Warren Buffett annual letter to Berkshire Hathaway shareholders, 1979

“Turnaround” here describes an attempt to save a once-successful business that ran into troubles. An attempt to turn the ship around and find a safe course before hitting an iceberg. Such was the case of Berkshire itself when Buffett started buying it in the 1960s. But let’s take a step back first.

Berkshire Hathaway was formed by the merger of Berkshire Cotton Manufacturing and Hathaway Mills, both founded in Massachusetts during the 1880s. The New England textile industry thrived during that period thanks to both the hydropower generated by the region’s strong rivers, and the naturally cool climate. These advantages, however, went away in the early 20th century, with the rise of steam power and air conditioning; processing cotton in the US South – the same location where the raw material was being produced – became a more compelling alternative versus transporting it to New England1.

In other words: the moat disappeared, and with it, Berkshire Hathaway’s ability to earn good returns on capital.

That was already the state of things when Buffett started buying Berkshire stock in 1962; despite the decline of textile in New England, Buffett was drawn to the low valuation, as he explained in his 1965 partnership letter:

Our purchases of Berkshire started at a price of $7.60 per share in 1962. This price partially reflected large losses incurred by the prior management in closing some of the mills made obsolete by changing conditions within the textile business (which the old management had been quite slow to recognize). In the postwar period the company had slid downhill a considerable distance, having hit a peak in 1948 when about $29 1/2 million was earned before tax and about 11,000 workers were employed. This reflected output from 11 mills.

At the time we acquired control in spring of 1965, Berkshire was down to two mills and about 2,300 employees. It was a very pleasant surprise to find that the remaining units had excellent management personnel, and we have not had to bring a single man from the outside into the operation. In relation to our beginning acquisition cost of $7.60 per share (the average cost, however, was $14.86 per share, reflecting very heavy purchases in early 1965), the company on December 31, 1965, had net working capital alone (before placing any value on the plants and equipment) of about $19 per share.

Berkshire is a delight to own. There is no question that the state of the textile industry is the dominant factor in determining the earning power of the business, but we are most fortunate to have Ken Chace running the business in a first-class manner, and we also have several of the best sales people in the business heading up this end of their respective divisions.

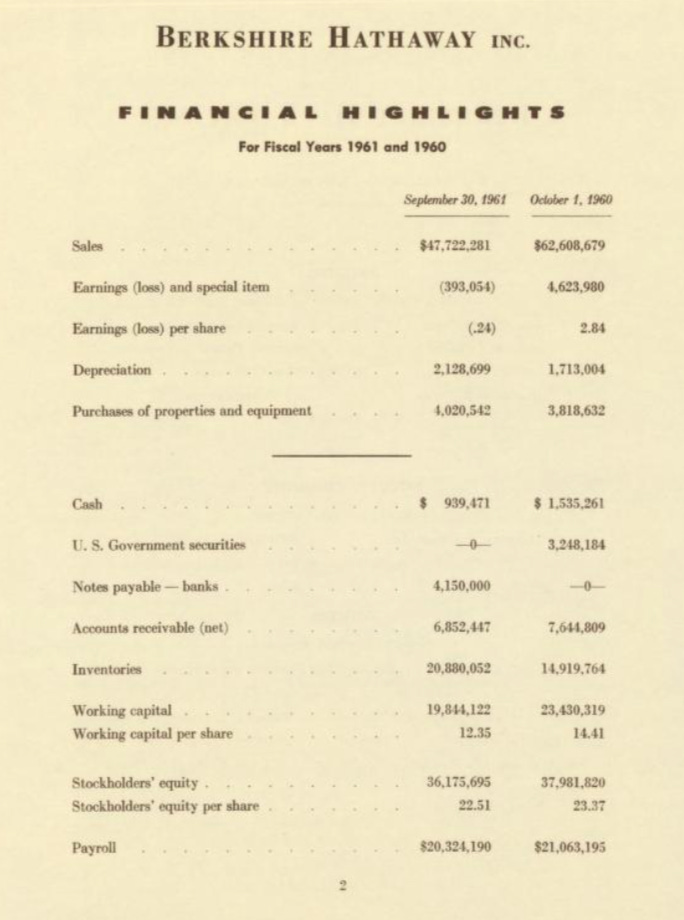

Berkshire Hathaway’s 1961 financials don’t seem particularly delightful – with declining sales, rising capital expenses, and a swing into net loss – but Buffett wasn’t blind to it; he was excited about buying it for less than its working capital, which means the investment could be profitable merely by shutting down the business, paying its obligations, and taking out whatever liquid assets are left. That wasn’t the plan though2, and Buffett trusted then-manager Ken Chace to preside over the process of liquidating unprofitable production lines, while squeezing whatever profits were possible from others.

It’s incredible how straight-forward Value Investing seemed in the early 1960s: the annual report literally tells you “working capital per share = $12.35”, and you could simply snatch up shares for $7.50. Buffett assumed control of Berkshire in 1965, and held onto his shares when his partnership shut down (and even bought more). The delight, however, didn’t last.

“The strategy was not ideal”

From Warren Buffett’s 1989 annual shareholder letter, under Mistakes of the First Twenty-Five Years:

My first mistake, of course, was in buying control of Berkshire. Though I knew its business - textile manufacturing - to be unpromising, I was enticed to buy because the price looked cheap. Stock purchases of that kind had proved reasonably rewarding in my early years, though by the time Berkshire came along in 1965 I was becoming aware that the strategy was not ideal.

Even by buying cheaply and having a superb manager, one cannot fight the rules of economics: in a competitive commodity market – which Berkshire’s cotton products very much were – price stabilizes at the marginal cost of the producer with the worst cost structure. Berkshire sold its cotton products for the same prices as cotton made in the south, but sustained higher costs compared to its southern competitors. While the low-cost producers generated profits, Berkshire struggled to do so.

The tragedy was that any investment in reducing its costs only made things worse, as Charlie Munger explained in his famous Art of Stock Picking speech:

The great lesson in microeconomics is to discriminate between when technology is going to help you and when it’s going to kill you. And most people do not get this straight in their heads. But a fellow like Buffett does.

For example, when we were in the textile business, which is a terrible commodity business, we were making low-end textiles which are a real commodity product. And one day, the people came to Warren and said, “They’ve invented a new loom that we think will do twice as much work as our old ones.”

And Warren said, “Gee, I hope this doesn’t work because if it does, I’m going to close the mill.” And he meant it.

What was he thinking? He was thinking, “It’s a lousy business. We’re earning substandard returns and keeping it open just to be nice to the elderly workers. But we’re not going to put huge amounts of new capital into a lousy business.”

And he knew that the huge productivity increases that would come from a better machine introduced into the production of a commodity product would all go to the benefit of the buyers of the textiles. Nothing was going to stick to our ribs as owners.

That’s such an obvious concept ‑ that there are all kinds of wonderful new inventions that give you nothing as owners except the opportunity to spend a lot more money in a business that’s still going to be lousy. The money still won’t come to you. All of the advantages from great improvements are going to flow through to the customers.

Such is life when a business with no moat operates in a competitive market. In a stark contrast, a business with a strong moat can earn wonderful returns on invested capital, as Buffett later learned from experience – here is Munger again:

Conversely, if you own the only newspaper in Oshkosh and they were to invent more efficient ways of composing the whole newspaper, then when you got rid of the old technology and got new fancy computers and so forth, all of the savings would come right through to the bottom line.

Luckily, Ken Chace understood his job at Berkshire: he shut down the commodity cotton production by 1969. Instead, he focused on niches where Berkshire still seemed to have had some pricing power. Buffett’s 1979 letter mentions the decorator line as “our strongest franchise”: these fabrics were used in furniture and home interiors, and required more sophisticated design, expertise, and relationships with customers. Not a pure commodity. But even there, Berkshire failed to develop a real moat or generate sustainable profits. By 1985, Buffett reported that he shut down the entire textile operation.

The cheap purchase price might have prevented Buffett from losing money on Berkshire (despite its poor business results), but the real loss – he explained – was the opportunity cost:

The same energies and talent are much better employed in a good business purchased at a fair price than in a poor business purchased at a bargain price.

Cigar-Butts and Value Traps

In 1989, Buffett articulated why it’s a mistake to buy into declining businesses with no moat, even if they trade for a bargain:

If you buy a stock at a sufficiently low price, there will usually be some hiccup in the fortunes of the business that gives you a chance to unload at a decent profit, even though the long-term performance of the business may be terrible. I call this the “cigar butt” approach to investing. A cigar butt found on the street that has only one puff left in it may not offer much of a smoke, but the “bargain purchase” will make that puff all profit.

Unless you are a liquidator, that kind of approach to buying businesses is foolish. First, the original “bargain” price probably will not turn out to be such a steal after all. In a difficult business, no sooner is one problem solved than another surfaces - never is there just one cockroach in the kitchen. Second, any initial advantage you secure will be quickly eroded by the low return that the business earns. For example, if you buy a business for $8 million that can be sold or liquidated for $10 million and promptly take either course, you can realize a high return. But the investment will disappoint if the business is sold for $10 million in ten years and in the interim has annually earned and distributed only a few percent on cost. Time is the friend of the wonderful business, the enemy of the mediocre.

But even though Buffett explained this business lesson so well over four decades ago, investors kept repeating this same mistake over and over again.

This lesson wasn’t specifically about textile mills. The simplified story of what happened to companies like IBM and Apple by the early 1990s, or BlackBerry and Yahoo in the early 2010s, or a bunch of others, is that they all lost their moats. Similar to Berkshire’s condition in 1965.

The stocks would, naturally, crash in response; perhaps more than deserved, as the stock market tends to overshoot in both directions. Even so, Buffett’s painful lesson is to stay away from businesses without a moat, no matter the price. And yet, the urge to invest in a seemingly-cheap stock can be hard for investors to resist. The thesis generally goes something like, “It used to be such a great business; yeah, they ran into some troubles, but the stock is a bargain at 9 times earnings – the new CEO seems great, surely they could do something!”

And a new CEO, talented and hard-working, is appointed to come up with a new strategy. The stock typically rises with optimism. But other than cutting costs through layoffs and project terminations, there is typically not much the new CEO can do in this situation. It’s not about the manager, Buffett explained, it’s the economics:

Good jockeys will do well on good horses, but not on broken-down nags [...] The same managers employed in a business with good economic characteristics would have achieved fine records. But they were never going to make any progress while running in quicksand.

[...]I’ve said many times that when a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact. I just wish I hadn’t been so energetic in creating examples.

A real turnaround requires growth, and while a fortunate hiccup may boost short-term revenue – making it seem as if the turnaround is working – durable and profitable growth is only achieved through an investment that could provide sustainable high returns on capital. And sustainable high returns on capital is impossible to achieve without a strong business moat.

When a business doesn’t have a moat, however, it requires almost a miracle to establish a new one. That’s what “new CEO” optimism tends to miss. Buffett mentioned how a lot of hard work went into figuring out Berkshire’s textile business, to no avail.

Some of these cases tend to draw inspiration from the miraculous turnaround Steve Jobs led upon returning to Apple in 1997, but that was the exception that proves the rule: it took a phenomenal leader like Steve Jobs (and, also, quite a bit of luck) to rebuild Apple’s moat3. These things only happen on rare occasions. Turnarounds seldom turn. Usually, they don’t. The hopeful CEO runs out of political capital within a few years, and is replaced by yet another potential “turnaround CEO”.

Investors typically bid up the stock again in these cases. But while some of them may be able to enjoy a free puff – take advantage of a fortunate hiccup to cash out at a profit – most will realize the same harsh lessons they could have learned by reading Buffett’s old letters: It’s better to pay up for a business that already has a wide and relevant moat, than to buy a cheap business without one, in hope that it could be developed.

Disclosure: Long BRK. Not financial advice. This post is for educational and general purposes only and should not be relied upon for investment decisions.

Moreover, workers in the south weren’t unionized, and therefore labor was cheaper compared to New England.

There were other non-economic considerations, as Buffett didn’t particularly enjoy laying people off; he wrote in 1969: “If we are not getting a good return on the textile business of Berkshire Hathaway Inc., why do we continue to operate it? Pretty much for the reasons outlined in my letter. I don't want to liquidate a business employing 1100 people when the Management has worked hard to improve their relative industry position, with reasonable results, and as long as the business does not require substantial additional capital investment. I have no desire to trade severe human dislocations for a few percentage points additional return per annum. Obviously, if we faced material compulsory additional investment or sustained operating losses, the decision might have to be different, but I don't anticipate such alternatives.”

This is also why other CEOs had previously failed in their attempts to save Apple.

עכשיו קראתי. יש הבחנה חשובה שכדאי לעשות - תפנית עסקית בהחלט יכולה להצליח במצבים מסויימים. כל ההתייחסויות של באפט ומאנגר המצוטטות במאמר מתייחסות למצבים בהם לעסק היה חפיר, והחפיר נעלם כתוצאה מתנאים חיצוניים, ואכן במצבים אלה אני מסכים לחלוטין.

בד בבד, יש מקרים רבים בהם החפיר נשחק כתוצאה מניהול לקוי, ושם החלפת ניהול בהחלט יכולה לייצר תפנית עסקית מוצלחת.

יותר מכך, במצבים האחרונים התשואות יכולות להיות מטורפות וגבוהות הרבה יותר מאשר בעסק צומח המנוהל היטב (ושנרכש במחיר הולם לאיכותו)

לא קראתי עדיין, אבל מעריך מאד הן את ההתעמקות בהיסטוריה (שאת זה גם אני אוהב לעשות ויודע כמה זה נדיר), את יכולת הכתיבה ועוד יותר מכך את הסבלנות לכתוב, שזה בחיים לא יהיה לי.