Monday's Retreat

Monday.com's recent strategy shift offers a fascinating peek into a potential disruption story unfolding in real-time.

Monday.com shares plummeted another 26% last week – down over 77% from last year’s highs, reaching an all-time-low – despite reporting strong overall numbers and rapid adoption of its AI initiatives.

Management highlighted continued upmarket momentum, while admitting to challenges around small business growth; that could be a bigger reason to worry than it might seem. While the sell-off could be attributed to the sector-wide AI Scare Trade, I think we might actually be seeing the early signs of actual disruption. Let me try to explain –

Choppiness

From co-founder & co-CEO Roy Mann prepared remarks on the recent earnings call:

In 2025 we continued to make meaningful progress winning further upmarket. Larger customers are increasingly standardizing on monday.com to support more complex critical workflows across their organizations. Customers with more than 50,000 in ARR now represent 41% of total ARR, reflecting strong expansion within existing accounts and success in landing larger, more strategic customers. At the high end, we delivered a record net adds of customers with over 100,000 plus in ARR. And customers with over $500,000 in ARR grew 74% year-over-year, underscoring our ability to support enterprise-scale deployments.

At the same time, no-touch channels continue to operate in a choppy demand environment, particularly among the smaller customers, which we expect to persist in 2026. What this means in practical terms is that the cost to acquire and expand self-serve customers has increased over the past year, and the returns on those investments have been below historical levels.

We do not see the same dynamic in our touch business, which has continued to accelerate in this past year. In response, we continued to shift investment to higher ROI opportunities that drive demand and success for larger customers. In addition, we continue to meaningfully improve the entire customer buying process, leveraging AI agents to improve conversion, adoption and engagement of all our customers.

The company then went on to spook investors by lowering growth expectations for 2026 and pulling back guidance for 2027; both were only first introduced on the September 2025 investor day. This might seem like Monday is out of touch with the market dynamics. Here is how CFO Eliran Glazer explained it:

Our confidence in the underlying fundamentals of the business and our long-term financial trajectory remains unchanged since our investor day in September. Given the evolving nature of the AI landscape, and the choppiness in the no-touch demand environment, we believe it is responsible to keep our near-term communication focused on what we can execute and deliver with high confidence. As a result, we will no longer be discussing our previously provided 2027 targets, but we’ll be centering our discussion on our 2026 outlook, which reflects the continued momentum we see across our AI work platform, new product introductions and upmarket sales motion. We remain committed to disciplined execution, which is consistent with our track record, and we will revisit long-term targets when there is greater visibility and it’s appropriate to do so.

If there’s “continued momentum across the AI work platform and upmarket sales motion”, though, why would there be “choppiness in the no-touch demand environment”?

The Monday Formula

‘No-touch’ refers to self-service onboarding. These are small customers—operations with just a few employees—who discover Monday.com after searching for ‘best work management tool’ and clicking a Google ad (or spotting it later on YouTube, Instagram, or LinkedIn).

What made this strategy so effective – and allowed Monday to economically outspend competitors like Asana or Smartsheet – was that people genuinely loved the product. Unlike tools such as Jira, which were designed by engineers for engineers and favored by IT departments, Monday enjoyed high adoption rates within the non-technical crowd. The combination of a highly calibrated direct marketing machine and a product with exceptional adoption rates is exactly what allowed Monday to break out and outgrow the competition.

Monday’s formula turned out to be best optimized for the SaaS era: focusing on user delight, rather than pleasing executives, and effectively leveraged product-led growth practices. To expand upmarket, Monday successfully layered a direct sales organization on top of its self-service ‘no-touch’ model. Positioning itself as a ‘Work OS,’ the company targeted the organizational ‘whitespace’ – business processes not addressed by a concrete SaaS tool.

While an overgeneralization, the enterprise SaaS industry can be thought of as Unbundling Microsoft Excel use cases (see previous article). Monday aimed at being the catch-all, a platform where non-tech-savvy corporate users could improvise software solutions – to streamline new employee onboarding, or manage a conference booth, for example – far more easily than they could with Excel.

Monday’s ‘Work OS’ unlocked so much ‘organizational whitespace’ that—beyond a thriving ecosystem of third-party extensions—the company began packaging its platform into dedicated products for specific verticals. Leveraging its data-driven DNA and strong design instincts, Monday drove significant adoption for its CRM, Dev (R&D management), and Service (IT & support) offerings, and expanded within larger and larger organizations.

Over the last three quarters, however, cracks have begun to appear at the bottom of the market: small businesses. “Only the S part of SMB,” as CFO Glazer put it. The ones acquired through ads and self-onboarding. Monday can no longer generate the high returns it once enjoyed from these channels.

Retreat

What makes the no-touch environment choppy?

For one, people aren’t searching for “best work management app” or “which crm should I use” and clicking on ads as much as they used to. They now receive an AI Overview, or even turn to their chatbot to begin with.

This drives an even deeper behavioral shift. Previously, users would click an ad, land on Monday.com, and convert based on its superb product experience. Now, they first engage in an analytical conversation with a chatbot1.

Monday’s core ‘you’ll feel it when you try it’ advantage doesn’t apply in a chat-based conversation. I tried asking three leading chatbots for the ‘best work management tool’ for a hypothetical small business. Interestingly, Notion was the top recommendation, and Monday appeared in only one response. As I elaborated about my pretend-business needs, the AI responded with bullet points and ‘pros & cons’ tables (e.g., ‘Use ClickUp for this, Trello if you prioritize that’). This is a return to the RFP-style logic-driven corporate buying process of the on-premise era, the exact opposite of the ‘try it and fall in love’ SaaS model in which Monday thrived.

To make matters worse, AI-native ‘vibe-coding’ tools – such as Lovable, Replit, and Base44 – are investing aggressively in online ads to grab market share (as we discussed in the context of Base44 and Wix). The rise of price-insensitive competitors who prioritize growth-at-all-costs is driving down the once-healthy returns Monday enjoyed in its no-touch channels.

It might not be an overfunded hype; these tools – or even Claude Code itself – can provide a decent Monday alternative, particularly for a small operation (for now). While it’s hard to imagine many mainstream companies switching from buying software to building their own (though this seems to be a current trend among San Francisco startups) — Monday’s key premise was allowing customers to “improvise” custom-tailored software solutions without writing code. Well, this is literally what vibe-coding tools enable. They are the ultimate no-code platforms. So much so, that building your own monday.com has become the ‘hello world’ of vibe coding2, as perfectly illustrated by this tweet from CNBC’s Deirdre Bosa:

While these new tools may not yet be considered ‘corporate-grade’, they seem to be good enough for self-consumption, or for a small business. Monday might have overshot that segment with the recent round of price increases. Small businesses are adopting a new reality, that Monday wasn’t built to dominate.

This is what distinguishes true disruption: whereas sustaining innovations make the incumbent’s products better, disruptive technologies require a different business model. One that the leading incumbents aren’t suited to develop; hence, The Innovator’s Dilemma.

Monday’s response is to pivot away from small business growth and focus on its upmarket opportunity; it’s just that, the choppiness might not stop at the low end of the market.

Mini-Mills

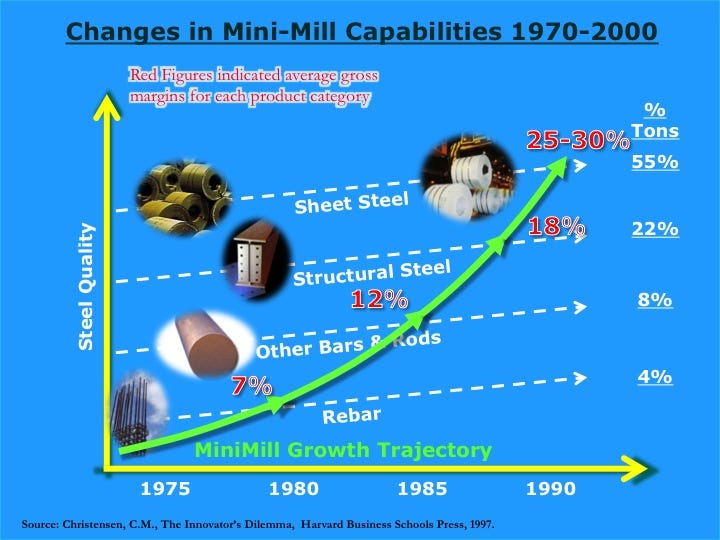

One thing that makes this so fascinating is how perfectly it fits the pattern that Prof. Clayton Christensen named ‘Disruption Theory’. Here is how he described – to Andy Grove and Intel’s management in late 1990s – how mini-mills disrupted the steel industry. From The New Yorker’s When Giants Fail:

[...] “Most of the world’s steel has been made by massive integrated steel companies. The other way to do it is to build a mini mill. In a mini mill, you melt scrap in electric furnaces, and you could easily fit four of them in this room. The most important thing about a mini mill is that you can make steel for twenty per cent lower cost than you can make it in an integrated mill [...]

“In the steel industry, as in your industry, there are tiers in the market,” he [Christensen] said. “At the bottom of the market is concrete reinforcing bar”—rebar. “Anyone can make rebar, but steel used to make appliances and cars”—sheet steel, at the top of the market—“is really tough to make. In the beginning, the mini mills were making steel from scrap, so the quality was crummy. The only market that would buy what the mini mills made was the rebar market, because there are almost no specs for rebar, and once you’ve buried it in cement you can’t verify if it made them anyway, so it was just the perfect market for a crummy product.

“As the mini mills attacked the rebar market, the reaction from the integrated mills was, man, they were happy to get out of rebar, because it was truly a dog-eat-dog commodity, and why would they ever want to defend the least profitable part of their business when, if they focussed their assets on angle iron and thicker bar and rod, the margins”—twelve per cent—“were so much better? So, as the mini mills expanded their capacity to make rebar, the integrated mills shut those lines down, and, as they chopped off the lowest-margin part of the product lines, their gross-margin profitability improved.”

That is the analogy to Monday’s retreat from the no-touch channels. The vibe-coding category resembles the steel mini-mills that utilized cheap technology to turn scrap into low-quality steel. It only makes sense to flee the bottom layer of the market and focus on the higher tiers, where the requirements are more complex – customers won’t settle for cheap steel made from scrap! – and the profit margins are higher. Alas, that strategy only worked for a short while; this is what happened next – back to Christensen:

[...] The integrated mills and the mini mills were happy with each other until 1979. “That was the year that the mini mills succeeded in driving the last of the integrated mills out of rebar,” Christensen said. “Bam!—the price of rebar collapsed by twenty per cent. It turned out that there was a subtle fact that nobody had thought about, and that is that a low-cost strategy only works when you have a high-cost competitor. As soon as the integrated mills fled upmarket, it was just low-cost mini mill fighting against low-cost mini mill. So what were these poor suckers going to do? One of them looked upmarket and said, ‘Holy cow, if we could make better steel, we could make money again!’ So they attacked the next tier of the market. And the integrated mills? Man, were they happy to wash their hands of that business. Because it was truly such a dog-eat-dog commodity business, and why would you ever defend a twelve-per-cent-margin business when you could focus your assets upmarket on structural steel, where the eighteen-per-cent margins were so much more attractive? And so the very same thing happened again. And as the integrated mills lopped off the lowest part of their product line their profitability improved.”

You can see where this is going. Over time, the integrated mills retreated to the very top of the market—until the mini-mills improved enough to capture that last layer (sheet steel). The integrated mills went bankrupt in the late 1990s.

To be clear, the integrated mills analogy isn’t perfect. Monday is not yet entrenched at the very top of the market, where giants like Salesforce and Microsoft still dominate. Instead, Monday has established a beachhead in the enterprise tier—large companies with relatively modest initial spend. The strategy now seems to be shifting growth budgets toward expanding these types of accounts, as CFO Eliran Glazer explained during the recent earnings call:

We’re not expecting to see a significant increase in the number of customers. We said it in the past, we have more than 250,000 customers, and we would like to extract our revenue within these customers. And we see this by our ACV actually growing, and we see bigger and more significant customers replacing the smaller customers.

How does Monday plan to extract more revenue from large enterprise customers? Here lies another key difference compared to the integrated mills: Monday isn’t ignoring AI, but rather embedding it throughout the product.

Monday users can use AI to automatically extract data from PDF files into a table, for example, or create workflows on top of their boards (a “board” is the atomic unit in monday.com, like a “sheet” in Excel). There is also Monday Vibe, where users can build apps powered by (and connected to) data stored on their boards. According to my brief testing, it wasn’t as good as Claude Code, but it is (1) tightly integrated with your existing data on Monday, and (2) it’s ‘enterprise-grade’ (whatever that means). Which makes it a great fit for the ‘expansion within existing enterprise customers’ strategy. Oh, and did I mention sidekick (which, if you squint, looks a lot like Microsoft Copilot) and Agent Factory (squint and it’s Salesforce’s Agentforce). All are essentially an attempt to turn AI into a sustaining technology with regards to Monday’s product, in the upper layers of the market.

While it may seem like a sound strategy for the short-to-medium term, the low-end choppiness is unlikely to subside, and unlikely to remain limited to the bottom of the market. Alongside Monday’s retreat, it reads like a textbook case of disruption in its early innings. The question now is whether Monday can entrench itself deeply enough before the “choppiness” escalates upmarket.

For new posts to land directly in your inbox:

Disclosure: not financial advice, this post is for educational and general purposes only and should not be relied upon for investment decisions.

Brian Chesky described the same phenomenon on a recent earnings call, where he explained why this is a positive for Airbnb.

credit: @YaronDav on X